BOISE, ID — A $50 U.S. savings bond discovered Tuesday in a shoebox at the back of Dale Hutchins’s hall closet has fully matured after 39 years, yielding a final redemption value of $73.92 — a figure his bank teller described as “technically correct.”

Hutchins, 61, located the bond while searching for his 2022 tax return. The certificate, issued in April 1987 by the U.S. Department of the Treasury and gifted to a then-22-year-old Dale by his grandmother Eunice, had been quietly compounding in the dark at an average annual rate that Hutchins’s wife Linda called “aspirational.”

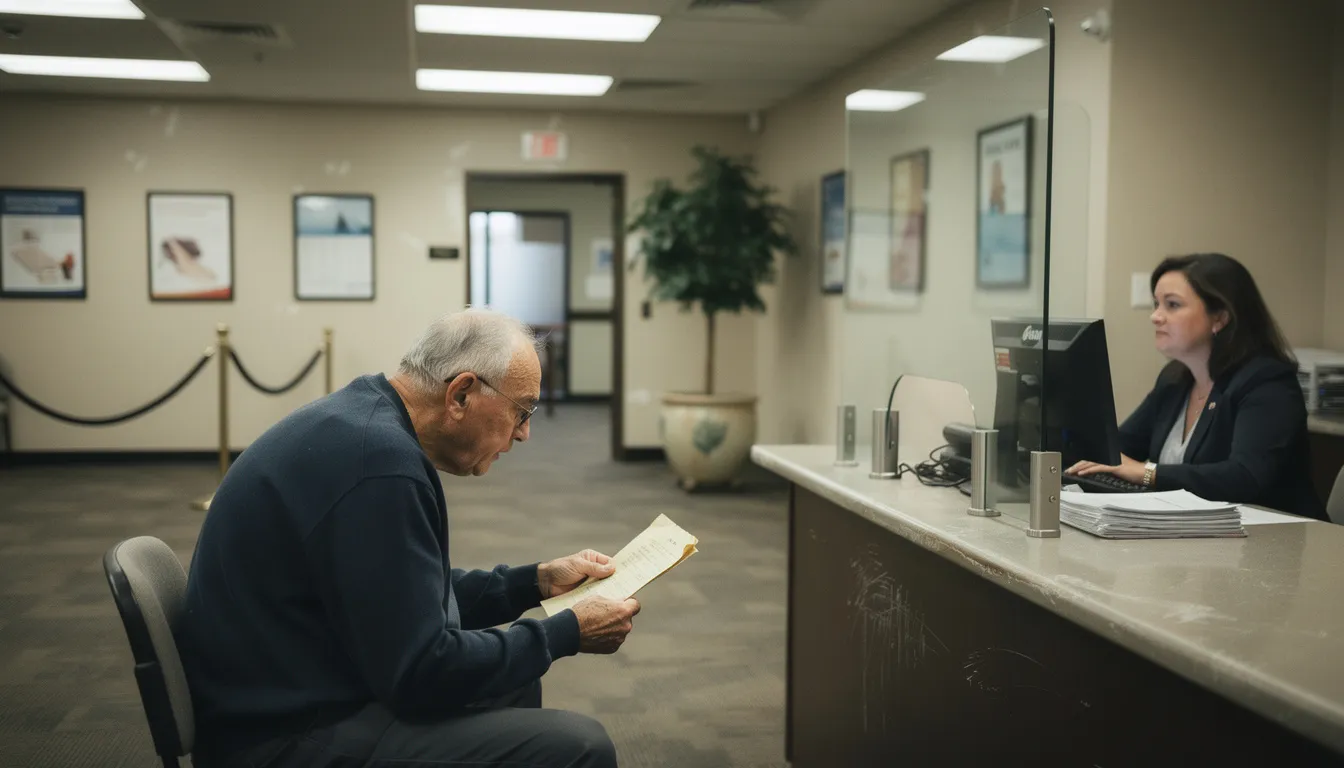

“Grandma Eunice always said this would really add up someday,” said Hutchins, standing in line at First Meridian Bank. “She was right. It added up $23.92. I’m going to frame the check.”

The redemption process required Hutchins to present two forms of ID, complete a Treasury form last revised during the Clinton administration, and wait 45 minutes while a branch manager located someone old enough to know what a savings bond was.

“The bond stopped earning interest in 2017, so technically he’s been losing ground to inflation for nine years. But the sentiment is really what matters here.”

“I see these maybe twice a year,” said First Meridian branch manager Carla Okonkwo, 44. “The bond stopped earning interest in 2017, so technically he’s been losing ground to inflation for nine years. But the sentiment is really what matters here.”

Hutchins confirmed he plans to deposit the $73.92 into a high-yield savings account currently offering 4.1% APY, where it will mature into approximately $76.00 by 2027.

At press time, Hutchins had located a second shoebox containing a $25 bond issued to his older brother Gary, who has been dead since 2009.